The IRS announced this morning that four Mississippi counties impacted by tornadoes have until July 31st to file. The extension, for Carroll, Humphreys, Monroe, and Sharkey counties, covers all tax forms and estimated tax payments due between now and July 30th for both business and individual returns. I would expect the Mississippi Department of Revenue to similarly extend their deadlines for impacted taxpayers.

Archive for the ‘IRS’ Category

Mississippi Counties Impacted by Tornadoes Have Until July 31st to File

Tuesday, March 28th, 2023Certain New York Storm Victims Get an Extra Month to File with the IRS

Friday, March 24th, 2023The IRS announced today that individuals (and businesses) in five New York counties have an extra month (to May 15th) to file and pay tax returns; this relates to the winter storm that hit between December 23rd and December 28th. The five counties are Erie, Genesee, Niagara, St. Lawrence, and Suffolk; the primary areas impacted are Buffalo/Niagara Falls and the east end of Long Island. This extension is automatic.

This extension includes business tax returns that were due in March and individual tax returns due in April and estimated payments due in April.

As of today, this relief is solely for federal (IRS) taxes. While I do expect the New York Department of Taxation and Finance to conform to this, they have yet to announce that they are conforming. UPDATE: New York state is not conforming to this extension!

The IRS announcement is here.

Today Is the Partnership & S-Corporation Deadline

Wednesday, March 15th, 2023You know what today is, right? Yes, the Ides of March–and the US tax filing deadline for partnerships and S-Corporations. If your entity isn’t ready to file, download Form 7004 (the extension request) and mail it using certified mail today. The deadline is a postmark deadline so it doesn’t matter when your extension is received–but you need to maintain proof of filing. Better yet, efile your extension and you don’t have to stand in line at the Post Office. (You can also send your extension via an IRS authorized private delivery service. Beware, not all offerings are authorized and it does matter.)

Most states piggyback onto the federal extension, but not all of them. New York, for example, requires a separate extension to be filed.

If you’re in most of California, you have an automatic extension until October 16th and you don’t have to send in an extension.

California (Franchise Tax Board) Conforms to Extension to October 16th

Friday, March 3rd, 2023The Franchise Tax Board announced late yesterday that California is officially conforming to the IRS extension until October 16th for all tax returns due from January 10th through October 15. Almost all of California is covered by the extension; only Imperial, Kern, Lassen, Modoc, Plumas, Shasta, and Sierra counties are not covered. (The largest cities which still have March, April, June, and September deadlines are Bakersfield, El Centro, and Redding.)

The extension covers:

- 4th quarter 2022 estimated payments due on January 17th;

- Partnership and S-Corporation returns due on March 15th;

- Individual, C-Corporation, and Trust/Estate returns due on April 17th;

- 1st, 2nd, and 3rd quarter 2023 estimated payments due on April 17th, June 15th, and September 15th; and

- Almost all other tax forms due before October 16th.

Individuals in the federal disaster area do not need to do anything to obtain an extension: It’s automatic. However, if you have moved from the area because you were impacted by the flooding or you reside outside of the area and were impacted and need the extension you do need to contact the IRS at 866-562-5227; I would also in such a situation contact the FTB.

IRS Extends California (and Alabama and Georgia) Disaster Areas to October 16th from May 15th

Friday, February 24th, 2023The IRS announced today that most California taxpayers (most of the state is in a disaster zone from flooding in January) now have until October 16th to file any tax returns. This also means that impacted taxpayers have until October 16th to make 2022 contributions for IRAs and HSAs. Additionally, 4th quarter 2022 and 1st and 2nd quarter 2023 estimated payments are now due on October 16th. California’s Franchise Tax Board normally conforms to all federal disaster extensions; I expect to see confirmation from the FTB by Monday.

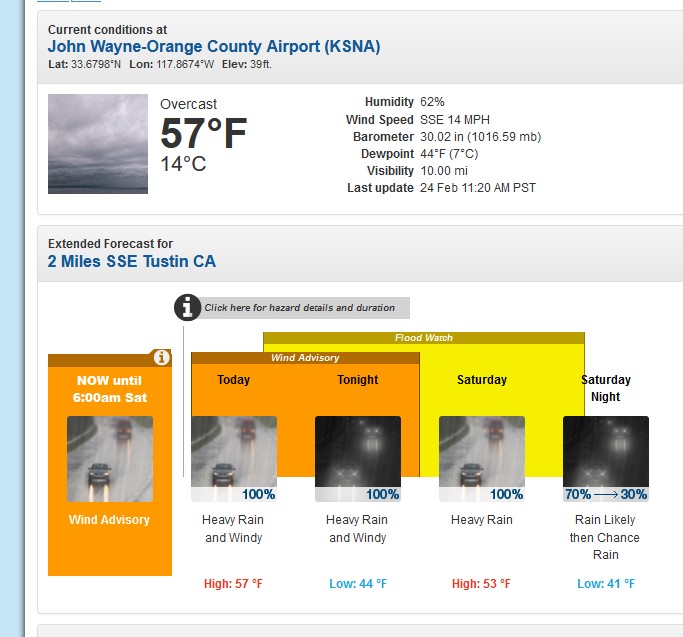

Meanwhile, California–especially Southern California–is bracing for more miserable weather. There are blizzard warnings (!) for the Southern California mountains, and my old homestead of Irvine (and most of Los Angeles-Orange Counties) is under a Flood Watch:

Here is the beginning of the IRS announcement:

Disaster-area taxpayers in most of California and parts of Alabama and Georgia now have until Oct. 16, 2023, to file various federal individual and business tax returns and make tax payments, the Internal Revenue Service announced today. Previously, the deadline had been postponed to May 15 for these areas.

The IRS is offering relief to any area designated by the Federal Emergency Management Agency (FEMA) in these three states. There are four different eligible FEMA declarations, and the start dates and other details vary for each of these disasters. The current list of eligible localities and other details for each disaster are always available on the disaster relief page on IRS.gov.

The additional relief postpones until Oct. 16, various tax filing and payment deadlines, including those for most calendar-year 2022 individual and business returns. This includes: Individual income tax returns, originally due on April 18; Various business returns, normally due on March 15 and April 18; and returns of tax-exempt organizations, normally due on May 15.

Among other things, this means that eligible taxpayers will also have until Oct. 16 to make 2022 contributions to their IRAs and health savings accounts.

In addition, farmers who choose to forgo making estimated tax payments and normally file their returns by March 1 will now have until Oct. 16, 2023, to file their 2022 return and pay any tax due.

The Oct. 16 deadline also applies to the estimated tax payment for the fourth quarter of 2022, originally due on Jan. 17, 2023. This means that taxpayers can skip making this payment and instead include it with the 2022 return they file, on or before Oct. 16.

The Oct. 16 deadline also applies to 2023 estimated tax payments, normally due on April 18, June 15 and Sept. 15. It also applies to the quarterly payroll and excise tax returns normally due on Jan. 31, April 30 and July 31.

The IRS disaster relief page has details on other returns, payments and tax-related actions qualifying for the additional time. Taxpayers in the affected areas do not need to file any extension paperwork, and they do not need to call the IRS to qualify for the extended time.

Good, Bad, and Ugly With the IRS

Thursday, February 9th, 2023This week I’ve had to call the IRS up for several different items. There is good news, bad news, and some ugly news.

The good news: In calling the Practitioner Priority Service (PPS), I’ve gotten through every time! Twice, there was no wait! I was disconnected once after reaching an agent but I called back and was immediately connected to another agent. For practitioners, this is great news and will make our lives easier in Tax Season.

The bad news: The IRS remains slow to respond to obvious issues. For example, the California “Middle Class Tax Rebates” were announced last year. California exempted them from state taxation (which is their right); how would they be treated for federal tax returns? There were (and are) two schools of thought: these are taxable as an accession to wealth or these are not taxable based on the “General Welfare” theory. A ruling from the IRS is due soon. My suspicion is that the IRS will rule that these aren’t taxed–based on politics, not law. (This isn’t just a California issue; several states enacted similar programs in 2022.)

The ugly news: Yesterday, I spoke with an IRS Appeals Officer on a case. We didn’t agree completely on my client’s issues, but we did agree on where to go to move the case forward. (Like almost everyone I have dealt with at the IRS, she was pleasant and helpful.) So why am I putting this in “ugly news?”

The issue is her workload. From everything I’ve seen, Appeals is buried (see below for another example of this). She confirmed this, and noted that over the past three years the number of Appeals Officers has decreased to a point that she thinks it will take five years to rebuild the staffing. (You can’t just hire effective Appeals Officers.) I agree–it will be years before this and other Pandemic-related backlogs are resolved.

Speaking of backlogs, paper remains the IRS’s Achilles heal. Here’s an example impacting a client of mine. An individual self-represented for an audit. That individual lost at the audit, hired me, and I requested an Appeals hearing by certified mail. That request was received timely (we tracked the mailing), and we received a notification that the file was sent to an IRS office. No matter, a Notice of Deficiency was issued so now my client must file a Tax Court petition because of an IRS error. If this ever goes to Tax Court (which isn’t likely–filing the petition will cause the case to be assigned to Appeals), I doubt the court would look favorably at the IRS ignoring its own procedures.

Additionally, yesterday I needed a transcript for a client. I went onto IRS E-Services to download it (I had an authorization sent to the IRS back in 2021) and it failed. Why? Who knows. I show it was successfully faxed–but it went into the ether.

As I noted above, it’s going to take years for the IRS to work its way out of the backlog and staffing issues. This isn’t just for Appeals, but for Exam (audit), collections, and all functions of the IRS. If there’s a budget shutdown or anything else like that, this could delay things even more.

Is It January 9th Yet?

Friday, January 20th, 2023Last year, the IRS announced a new system for efiling 1099s (and other information returns) called IRIS. This system would be available for both professionals and individuals (and businesses) to efile 1099s. The system was supposed to be available on January 9th. On January 9th the webpage noted, “…[Y]ou can log in to IRIS starting mid-January 2023.” Well, today is January 20th and the system still isn’t available.

(I do need to note you must have an IRS IRIS Transmitter Control Code (TCC) to use IRIS. You can apply for one via a link on the IRIS webpage.)

The deadline for mailing most information returns remains January 31st–and that’s 21 days away. We are back using the IRS FIRE system (this system is not available to the general public) for one more year as it appears we have no options. There are many services you can find that will file 1099s, but we have batches of 1099s for our clients that need filing.

Perhaps the original announcement of the IRIS system was correct: the IRS simply didn’t note which year the system would be up on. After all, there’s a January 9th in 2024, too.

UPDATE: The IRS’s IRIS system went live earlier this week.

Start Your 2023 Mileage Log

Tuesday, January 3rd, 2023I’m going to start the new year with a couple reposts of essential information. Yes, you do need to keep a mileage log:

Tuesday will be the first business day of the new year for many. You may have resolved to keep good records this year (at least, we hope you have). Start with keeping an accurate, contemporaneous written mileage log (or use a smart phone app–with periodic sending of the information to yourself to prove that the log is contemporaneous).

Why, you ask? Because if you want to deduct all of your business mileage, you must do this! IRS regulations and Tax Court rulings require this. Written is defined as ink, so that means you need a paper log or must be able to prove your smart phone log is contemporaneous.

The first step is to go out to your car, and note the starting mileage for the new year. So go out to your car, and jot down that number (mine was 123,808). That should be the first entry in your mileage log. I use a small memo book for my mileage log; it conveniently fits in the center console of my car. It’s also a good idea to take a picture of the odometer and email that picture to yourself. This will give you a time-stamp showing you accurately noted your beginning mileage.

Here’s the other things you should do:

On the cover of your log, write “2023 Mileage Log for [Your Name].”

Each time you drive for business, note the date, the starting and ending mileage, where you went, and the business purpose. Let’s say you drive to meet a new client, and meet him at his business. The entry might look like:

1/4 123900-123935 Office-Acme Products (1234 Main St, Las Vegas)-Office, Discuss requirements for preparing tax return, year-end journal entries.

It takes just a few seconds to do this after each trip, and with the standard mileage rate being $0.655/mile, the 35 miles in this hypothetical trip would be worth a deduction of $23. That deduction does add up.

Some gotchas and questions:

1. Why not use a smartphone app? Actually, you can but the current regulations require you to also keep a written mileage log. You can transfer your computer app nightly to paper, and that way you can have the best of both worlds. Unfortunately, current regulations do not guarantee that a phone app will be accepted by the IRS in an audit.

That said, if you backup (or transfer) your phone app on a regular basis, and can then print out those backups, that should work. The regular backups should have identical historical information; the information can then be printed and will function as a written mileage log. I do need to point out that the Tax Court has not specifically looked at mileage logs maintained on a phone. A written mileage log (pen and paper) will be accepted; a phone app with backups should be accepted.

2. I have a second car that I use just for my business. I don’t need a mileage log. Wrong. First, IRS regulations require documentation for your business miles; an auditor will not accept that 100% of the mileage is for business–you must prove it. Second, there will always be non-business miles. When you drive your car in for service, that’s not business miles; when you fill it up with gasoline, that’s not necessarily business miles. I’ve represented taxpayers in examinations without a written mileage log; trust me, it goes far, far easier when you have one.

3. Why do I need to record the starting miles for the year? There are two reasons. First, the IRS requires you to note the total miles driven for the year. The easiest way is to note the mileage at the beginning of the year. Second, if you want to deduct your mileage using actual expenses (rather than the standard mileage deduction), the calculation involves taking a ratio of business miles to actual miles.

4. Can I use actual expenses? Yes. You would need to record all of your expenses for your car: gas, oil, maintenance, repairs, insurance, registration, lease fees (or interest and depreciation), etc., and the deduction is figured by taking the sum of your expenses and multiplying by the percentage use of your car for business (business mileage to total mileage driven). Note that once you start using actual expenses for your car, you generally must continue with actual expenses for the life of the car. Be careful if you (or your family) have multiple vehicles. You will need to separate out your expenses by vehicle.

So start that mileage log today. And yes, your trip to the office supply store to buy a small memo pad is business miles that can be deducted.

2023 Standard Mileage Rates

Sunday, January 1st, 2023The IRS announced on December 29th the standard mileage rates:

- $0.665/mile for business use (up from $0.635/mile as of July 1, 2022);

- $0.22/mile for medical/moving for active-duty members of the Armed Forces; and

- $0.14/mile in service of charitable organizations.

These rates do apply to electric and hybrid vehicles along with gasoline and diesel vehicles.